A new report by blockchain research firm Chainalysis underscores Nigeria’s crypto adoption, ranking it second in its Global Adoption Index. Between July 2023 and June 2024, Nigeria received an impressive $59 billion in cryptocurrency transactions, marking a 4.06% increase compared to the previous year.

But what is fueling this surge in crypto usage in Africa’s most populous nation? And how has Nigeria become a leader in crypto adoption despite a rocky relationship with digital assets? This is a story of necessity, resilience, and innovation. Read on.

Nigeria’s Crypto Adoption in the Face of Economic Crisis

Nigeria’s economy, like many across Sub-Saharan Africa, is facing significant challenges. One of the major issues is a foreign exchange (FX) shortage that has left businesses scrambling for U.S. dollars, a critical currency for international trade. Chris Maurice, CEO of Yellow Card, a leading cryptocurrency platform, summed up the situation: “About 70 percent of African countries are facing an FX shortage, and businesses are struggling to get access to the dollars they need to operate.”

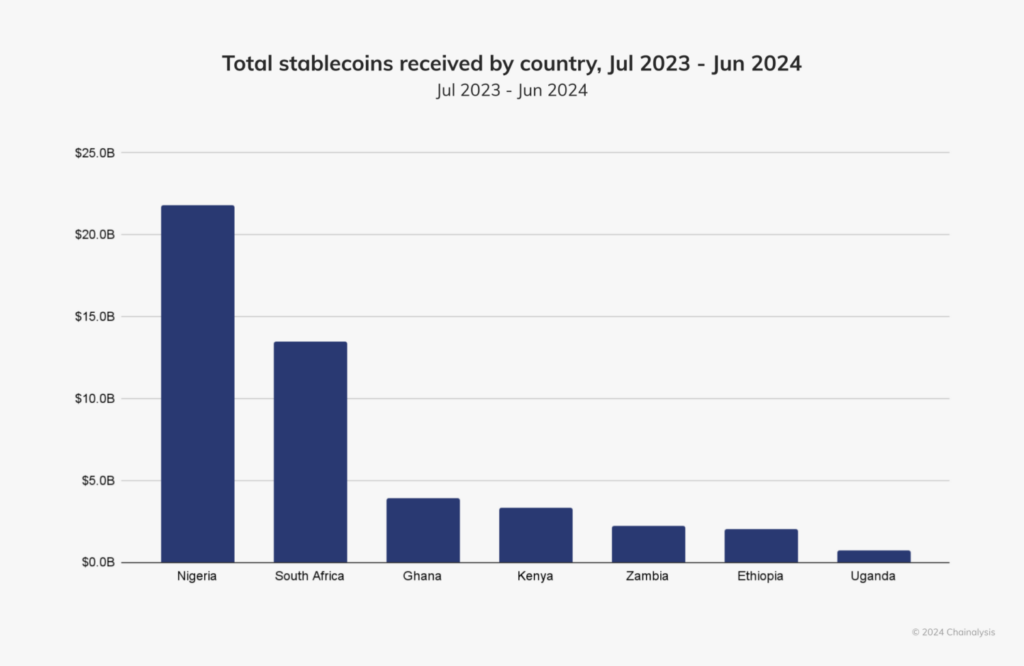

The lack of access to dollars has driven many Nigerians to explore alternatives, and cryptocurrencies have emerged as a viable solution. Stablecoins, particularly, have become a cornerstone of Nigeria’s crypto economy. These digital currencies pegged to stable assets like the U.S. dollar, offer Nigerians a way to conduct cross-border transactions efficiently and affordably. According to Chainalysis, stablecoins account for 40% of all crypto inflows into Nigeria.

With traditional banks and financial systems faltering, cryptocurrency has stepped in to bridge the gap. As Maurice notes, “The banks don’t have dollars, the government doesn’t have dollars, and even if they did, they wouldn’t give them to you.”

Faced with this reality, Nigerians increasingly rely on digital currencies not just as speculative investments but as tools for survival.

A Shift in Perception: From Speculation to Utility

One of the most significant changes in Nigeria’s cryptocurrency landscape is the evolving perception of digital assets. Initially seen as a “get-rich-quick” scheme, cryptocurrencies are now being recognized for their practical uses. Moyo Sodipo, the Chief Operating Officer of Busha, a Nigerian crypto exchange, explained that people are “starting to see the real-world utility of cryptocurrency, especially in day-to-day transactions.”

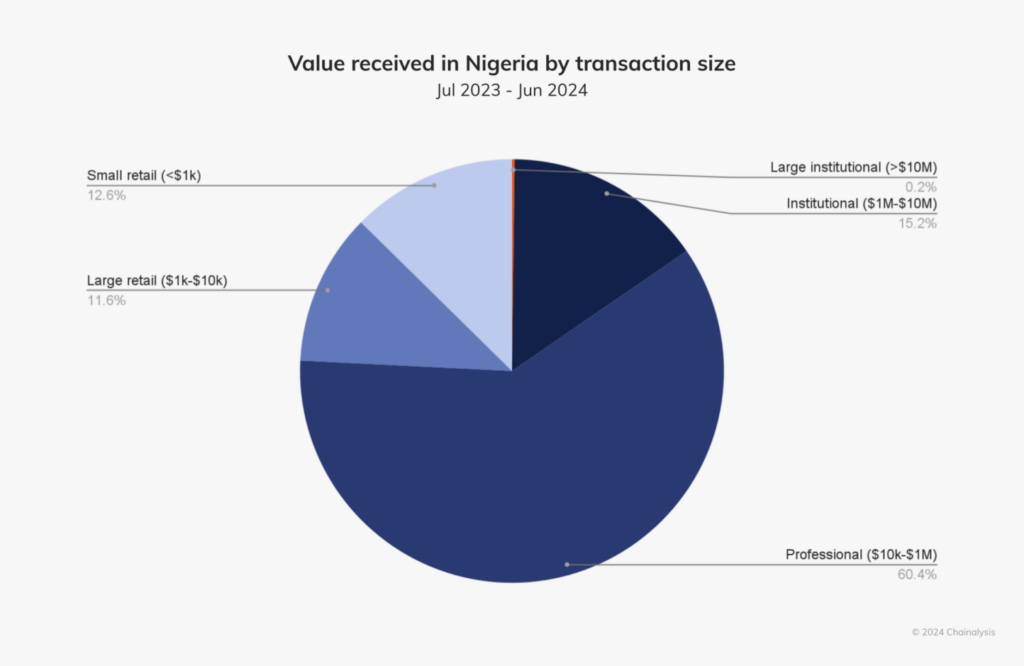

Indeed, cryptocurrency is no longer just a novelty for tech enthusiasts or financial adventurers. It has become an essential part of the financial toolkit for many Nigerians. Retail transactions—transfers valued at under $1 million—make up around 85% of Nigeria’s cryptocurrency activity. From buying groceries to paying for services, Nigerians are leveraging crypto to navigate a challenging economic environment.

Cross-Border Transactions: Stablecoins to the Rescue

One of the key areas where cryptocurrency is making a difference in Nigeria is in remittances. For years, traditional remittance channels have been inefficient and costly, with high fees and slow processing times. This has been especially frustrating for Nigerians who rely on money sent from abroad to support their families.

Enter stablecoins. As Sodipo of Busha points out, “Cross-border remittances are a major use case for stablecoins in Nigeria. It’s much faster and more affordable.” By bypassing traditional financial systems, stablecoins allow Nigerians to send and receive money from across borders with minimal fees and in a fraction of the time.

Regulating Nigeria’s crypto Adoption: A Tug of War Between Government and Innovation

Despite the obvious benefits, Nigeria’s government has had a complicated relationship with cryptocurrency. In 2024, the Central Bank of Nigeria (CBN) cracked down on crypto platforms, accusing them of manipulating exchange rates and aiding illicit financial flows. The government even instructed telecommunications companies to restrict access to platforms like Binance, further attempting to curb crypto transactions.

Yet, Nigeria’s crypto adoption has proven resilient. And as the industry continues to grow, the government’s stance appears to be softening.

In a surprising turn, Zacch Adedeji, chairman of the Federal Inland Revenue Service (FIRS), recently acknowledged the inevitability of cryptocurrency in Nigeria’s economy. “We cannot run away from the cryptocurrency ecosystem because it is the in-thing,” he admitts.

Thankfully, the Nigerian Securities Exchange Commission (SEC) has already begun to approve principles for crypto operators. This shift has been welcomed by industry leaders. As Sodipo noted, “The industry is bullish on Accelerated Regulation Incubation Program (one of SEC’s regulatory frameworks); it’s a shift away from uncertainty and a positive move towards regulatory clarity.”

The Road Ahead: Crypto’s Role in Nigeria’s Future

Nigeria’s embrace of cryptocurrency is a testament to the power of innovation in the face of adversity. In a country where traditional financial systems are struggling to meet the needs of the population, digital currencies have provided an alternative—a lifeline for individuals and businesses alike.

As Nigeria continues to navigate its economic challenges, cryptocurrency will undoubtedly play an increasingly important role in its financial landscape. Whether through stablecoins enabling cross-border remittances or blockchain-based solutions providing transparency in real estate and business transactions, the crypto revolution in Nigeria is just beginning.

And with the government’s evolving stance on regulation, the future looks even brighter for crypto in Nigeria. As Adedeji remarks, “We need a law that regulates that area of our economy.”

For Nigeria, cryptocurrency isn’t just a trend—it’s becoming a cornerstone of financial survival and growth.

Visits: 52